Final Thoughts

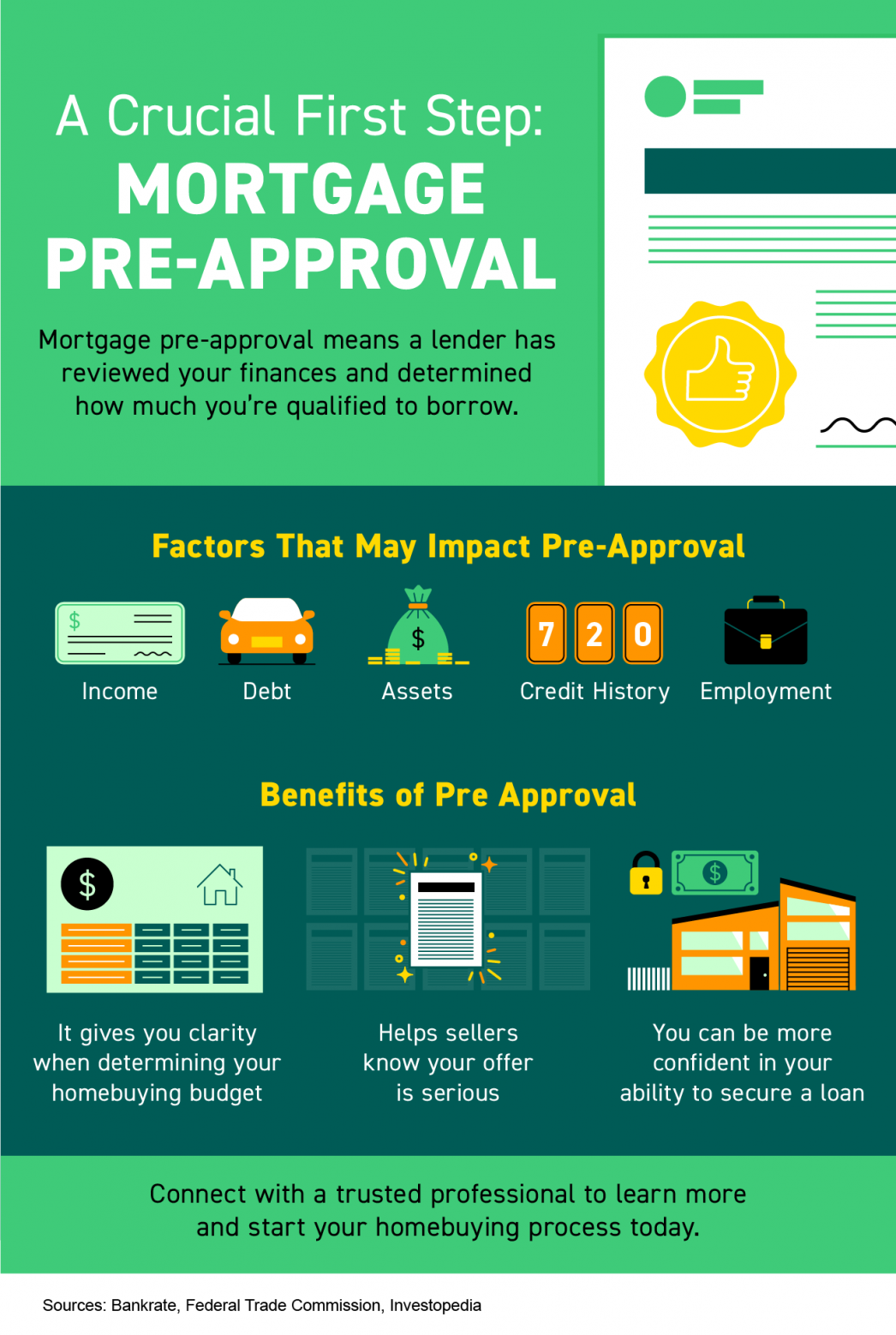

Getting mortgage pre-approval before you start house hunting isn't just smart advice – it's your foundation for making confident decisions in a competitive market. We've covered why browsing listings without knowing your financial limits leads to wasted time and heartbreak, how pre-approval differs from pre-qualification, and the strategic advantages of understanding your budget early.

This approach transforms your entire home-buying experience. Instead of falling in love with homes you can't afford, you'll search within realistic parameters. When you find the right property, you can move quickly with an offer that sellers take seriously. Pre-approval also gives you flexibility if your timeline changes, since most approvals stay valid for 60 to 90 days.

The fear that pre-approval locks you into immediate commitment is unfounded. You're not obligated to use that lender or buy a home right away. You're simply gathering crucial information that helps you make better choices throughout the process.

Your financial readiness determines everything else – from which neighborhoods to consider to how aggressively you can negotiate. Without this knowledge, you're essentially shopping blindfolded in one of the biggest purchases of your life.

Stop scrolling through listings and start with the numbers that matter. Contact a mortgage lender this week to begin your pre-approval process. Gather your recent pay stubs, tax returns, and bank statements. Once you have that pre-approval letter in hand, you'll search for homes with purpose and confidence instead of hope and guesswork.

Check out this article next